12. Sequence risk#

12.1. Introduction#

Sequence risk occurs when investment or withdrawal is distributed in time. These two scenarios may be representative of:

Dollar Cost Averaging (DCA, or PAC in Italian for “Piano di Accumulo di Capitale”)

Withdrawal during old age

Sequence in time of 1-period returns may strongly influence the composite return of a portfolio.

12.1.1. Mathematical model#

In a continuous-time model, sequence risk of constant-amount DCA or withdrawal can be modeled with a Goemetric Brownian Motion with “drift”,

being \(C_t\) the rate of investment (\(> 0\)) or withdrawal (\(< 0\)), \(\mu\), \(\sigma\) the expected value and variance of the rate of return. A discrete-time counterpart may be

with \(\mu_{n,n+1}\), \(\sigma_{n,n+1}\) the expected value and the variance of the 1-period return, \(W_{n,n+1}\) a unit-variance random variable representing the distribution of the returns from \(n\) to \(n+1\), and \(C_{n,n+1}\) the investment of withdrawal from \(n\) to \(n+1\).

12.1.2. Constant investment or withdrawal rate: analytical solution#

The solution of the continuous-time equation with reads

12.2. Realizations#

12.2.1. Libraries and parameters#

Show code cell source

import numpy as np

import matplotlib.pyplot as plt

#> Parameters

# E.g. Portfolio with 1-year return with expected value and variance 8%, 15%,

# 1-period withdrawal .04,, and initial value of the portfolio 1., like

# 40k€ withdrawal of an initial portfolio of 1M€

wealth_ruin_exp = -3

#> Random number generator, representing 1-period return R_n = Y_{n}/Y_{n-1}

nreal = 2000 # n. of realizations of the random process

nt = 100 # n. of periods (toss) for each realization

tv = np.arange(nt)

#> Random number generators of the 2 assets

rng = np.random.default_rng().normal

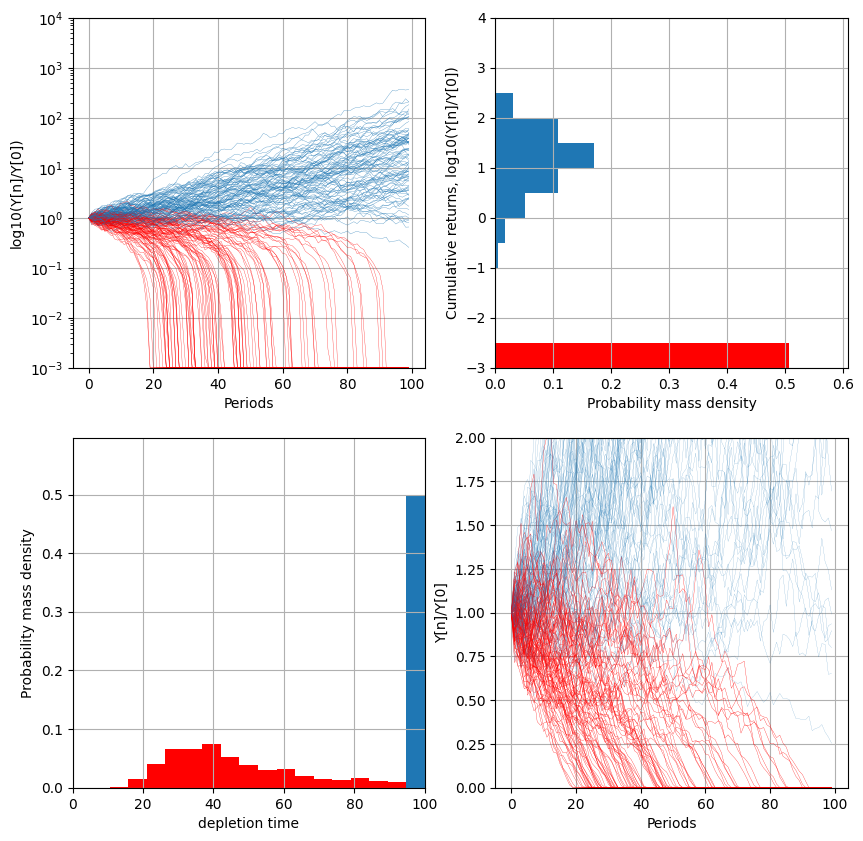

12.2.2. Constant Withdrawals#

Show code cell source

#> Parameters

mu, sigma, C = .045, .10, -.04

x0 = 1.

rng_params = {'loc': mu, 'scale': sigma, 'size': nt}

#> End values, max drawdowns

x_end = np.zeros(nreal)

depletion_times = np.zeros(nreal)

n_ruins = 0

fig, ax = plt.subplots(2,2, figsize=(10, 10))

for ireal in np.arange(nreal):

#> 1-period returns of the 2 assets

r = rng(**rng_params)

#> Rebalanced portfolio

x = np.zeros(nt); x[0] = x0

for ix in np.arange(1,nt):

x[ix] = x[ix-1] + r[ix-1] * x[ix-1] + C

#> Ruin condition, when portfolio goes to zero

neg_indices = np.where(x < 0)[0]

if ( neg_indices.size > 0 ):

time_of_depletion = neg_indices[0]

x[time_of_depletion:] = x0 * 10**wealth_ruin_exp

n_ruins += 1

else:

time_of_depletion = nt

#> End values

x_end[ireal] = x[-1]

depletion_times[ireal] = time_of_depletion

#> Plot time-history

if ( ireal % 10 == 0 ):

lw = .2 #

color = plt.cm.tab10.colors[0] if time_of_depletion == nt else 'red'

ax[0,0].semilogy(tv, x/x[0], color=color, lw=lw) # , color=plt.cm.tab10.colors[0])

ax[1,1].plot(tv, x/x[0], color=color, lw=.1 * ( time_of_depletion == nt ) + .2 * ( time_of_depletion < nt ))

#> Exponents of 10 of cumulative return for plots

minret_plot = wealth_ruin_exp

maxret_plot = np.ceil( (mu-sigma**2/2)*nt * 2 * np.log10(np.exp(1)) )

ax[0,0].set_ylabel("log10(Y[n]/Y[0])")

ax[0,0].set_xlabel("Periods")

ax[0,0].set_ylim([10**minret_plot, 10**maxret_plot]) # e^at = (10^(log10(e)))^at

ax[0,0].grid()

dbins = .5

bins = np.arange(minret_plot, maxret_plot, dbins)

counts, bins, patches = ax[0,1].hist(np.log10(x_end), bins=bins, orientation='horizontal', density=False)

# Modify hist() patches to get probability of ranges, like a discrete r.v.

total_count = counts.sum()

probs = counts/total_count

for prob, patch in zip(probs, patches):

patch.set_width(prob)

patches[0].set_facecolor('red')

ax[0,1].set_ylabel("Cumulative returns, log10(Y[n]/Y[0])")

ax[0,1].set_xlabel("Probability mass density")

ax[0,1].set_xlim([0,1.2 * np.max(probs)])

ax[0,1].set_ylim([minret_plot, maxret_plot])

ax[0,1].grid()

counts, bins, patches = ax[1,0].hist(depletion_times, bins=np.linspace(0,nt,20), density=False, color='red')

ax[1,0].set_ylabel("Probability mass density")

ax[1,0].set_xlabel("depletion time")

ax[1,0].grid()

total_count = counts.sum()

probs = counts/total_count

for prob, patch in zip(probs, patches):

patch.set_height(prob)

patches[-1].set_facecolor(plt.cm.tab10.colors[0])

ax[1,0].set_xlim([0, nt])

ax[1,0].set_ylim([0, 1.2*np.max(probs)])

ax[1,1].set_ylabel("Y[n]/Y[0]")

ax[1,1].set_xlabel("Periods")

ax[1,1].set_ylim([0, 2*x0]) # e^at = (10^(log10(e)))^at

ax[1,1].grid()

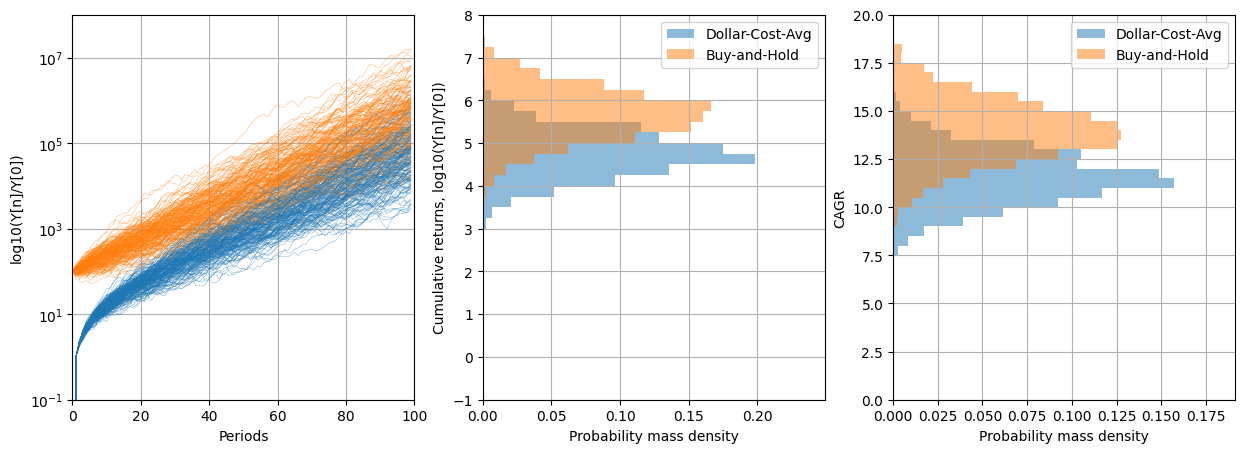

12.2.3. Dollar Cost Averaging (DCA)#

Show code cell source

#> Parameters

mu, sigma, C = .10, .15, .04

x0 = .0

x0_bah = C * nt

rng_params = {'loc': mu, 'scale': sigma, 'size': nt}

#> End values, max drawdowns

x_end = np.zeros(nreal) # Dollar-Cost-Avg (DCA), Ita: PAC

x_bah_end = np.zeros(nreal) # Buy-and-Hold (BAH) , Ita: PIC

fig, ax = plt.subplots(1,3, figsize=(15, 5))

for ireal in np.arange(nreal):

#> 1-period returns of the 2 assets

r = rng(**rng_params)

#> Rebalanced portfolio

x = np.zeros(nt); x[0] = x0

for ix in np.arange(1,nt):

x[ix] = x[ix-1] + r[ix-1] * x[ix-1] + C

x_bah = np.zeros(nt); x_bah[0] = x0_bah

x_bah[1:] = x_bah[0] * np.cumprod(1+r[1:])

#> End values

x_end[ireal] = x[-1]

x_bah_end[ireal] = x_bah[-1]

#> Plot time-history

if ( ireal % 10 == 0 ):

ax[0].semilogy(tv, x/C, lw=.2 , color=plt.cm.tab10.colors[0])

ax[0].semilogy(tv, x_bah/C, lw=.2 , color=plt.cm.tab10.colors[1])

#> Exponents of 10 of cumulative return for plots

minret_plot = -1

maxret_plot = np.ceil( (mu-sigma**2/2)*nt * 2. * np.log10(np.exp(1)) )

ax[0].set_ylabel("log10(Y[n]/Y[0])")

ax[0].set_xlabel("Periods")

ax[0].set_xlim([0, nt])

ax[0].set_ylim([10**minret_plot, 10**maxret_plot]) # e^at = (10^(log10(e)))^at

ax[0].grid()

dbins = .25

bins = np.arange(minret_plot, maxret_plot, dbins)

counts, bins, patches = ax[1].hist(np.log10(x_end/C), bins=bins, orientation='horizontal', density=False, color=plt.cm.tab10.colors[0], alpha=.5, label='Dollar-Cost-Avg')

# Modify hist() patches to get probability of ranges, like a discrete r.v.

total_count = counts.sum()

probs = counts/total_count

for prob, patch in zip(probs, patches):

patch.set_width(prob)

counts, bins, patches = ax[1].hist(np.log10(x_bah_end/C), bins=bins, orientation='horizontal', density=False, color=plt.cm.tab10.colors[1], alpha=.5, label='Buy-and-Hold')

# Modify hist() patches to get probability of ranges, like a discrete r.v.

total_count = counts.sum()

probs = counts/total_count

for prob, patch in zip(probs, patches):

patch.set_width(prob)

ax[1].set_ylabel("Cumulative returns, log10(Y[n]/Y[0])")

ax[1].set_xlabel("Probability mass density")

ax[1].set_xlim([0,1.5 * np.max(probs)])

ax[1].set_ylim([minret_plot, maxret_plot])

ax[1].legend()

ax[1].grid()

#>

dbins = .5

bins = np.arange(0.,30.,dbins)

counts, bins, patches = ax[2].hist(((x_end/C)**(1/nt)-1)*100, bins=bins, orientation='horizontal', density=False, color=plt.cm.tab10.colors[0], alpha=.5, label='Dollar-Cost-Avg')

# Modify hist() patches to get probability of ranges, like a discrete r.v.

total_count = counts.sum()

probs = counts/total_count

for prob, patch in zip(probs, patches):

patch.set_width(prob)

counts, bins, patches = ax[2].hist(((x_bah_end/C)**(1/nt)-1)*100, bins=bins, orientation='horizontal', density=False, color=plt.cm.tab10.colors[1], alpha=.5, label='Buy-and-Hold')

# Modify hist() patches to get probability of ranges, like a discrete r.v.

total_count = counts.sum()

probs = counts/total_count

for prob, patch in zip(probs, patches):

patch.set_width(prob)

ax[2].set_ylabel("CAGR")

ax[2].set_xlabel("Probability mass density")

ax[2].set_xlim([0, 1.5*np.max(probs)])

ax[2].set_ylim([0, 20])

ax[2].legend()

ax[2].grid()