20. Rebalancing#

In this Notwbook, two strategies on a 2-asset portfolio are discussed and compared:

rebalanced portfolio, after each period

buy-and-hold portfolio, without rebalancing

Effects of rebalancing and conditions for rebalancing premium are discussed: sometimes the expected log-return of the rebalanced portfolio may exceed the expected log-return of each single asset.

20.1. Libraries, parameters and useful functions#

Libraries are imported and useful functions to treat conics below are defined here

20.1.1. Libraries#

Show code cell content

import numpy as np

import matplotlib.pyplot as plt

from ipywidgets import interact, FloatSlider

20.1.2. Parameters#

Show code cell content

#>

params = {

'2-asset-portfolio': { 'mu1': .10, 'sigma1': .20, 'mu2': .08, 'sigma2': .15, 'rho': -.25}

}

20.1.3. Functions for conics#

Show code cell content

def conics_points(a,b,c,d,e,f,n=100,printout=False):

""" ax^2 + bxy + cy^2 + dx + ey + f = 0 """

delta = b**2 - 4*a*c

if delta == 0.: # possible parabola (comparison with reals?)

ctype = 'parabola'

x,y = np.zeros(n+1)

elif delta < 0.: # possible ellipse

ctype = 'ellipse'

x,y = ellipse_points(a,b,c,d,e,f,n,printout)

else: # possible hyperbola

ctype = 'hyperbola'

x,y = np.zeros(n+1)

return ctype, x, y

def ellipse_points(a,b,c,d,e,f,n=100,printout=False):

""" """

theta = np.pi / 4. * ( a == c ) + .5 * np.arctan2(b,a-c) * ( not a == c )

if printout: print(f"theta: {theta}")

A = a * ( np.cos(theta) )**2 + b * np.cos(theta) * np.sin(theta) + c * ( np.sin(theta) )**2

B = ( c - a ) * np.sin(2*theta) + b * np.cos(2*theta)

C = a * ( np.sin(theta) )**2 - b * np.cos(theta) * np.sin(theta) + c * ( np.cos(theta) )**2

D = d * np.cos(theta) + e * np.sin(theta)

E = -d * np.sin(theta) + e * np.cos(theta)

F = f

if ( A < 0 and C < 0 ):

A = -A; B = -B; C = -C; D = -D; E = -E; F = -F

elif ( A == 0 ) : raise ValueError("A = 0")

elif ( C == 0 ) : raise ValueError("C = 0")

elif ( A*C < 0. ): raise ValueError(f"A*C={A*C} <= 0")

uc = - .5 * D / A

vc = - .5 * E / C

FF = A * uc**2 + C * vc**2 - F

if printout: print(f"uc: {uc}\nvc: {vc}\nFF: {FF}")

if FF > 0:

if printout: print(f"A: {A}\nB: {B}\nC: {C}\nD: {D}\nE: {E}\nF: {F}")

semi_a = np.sqrt(FF/A)

semi_b = np.sqrt(FF/C)

if printout: print(f"semi_a: {semi_a}\nsemi_b: {semi_b}")

thv = np.linspace(0, 2*np.pi, n+1); thv[-1] = thv[0]

u, v = semi_a * np.cos(thv), semi_b * np.sin(thv)

x = ( u + uc ) * np.cos(theta) - ( v + vc ) * np.sin(theta)

y = ( u + uc ) * np.sin(theta) + ( v + vc ) * np.cos(theta)

return x,y

else:

raise ValueError(f"FF:{FF} <= 0")

# else: 0: degenerate ellipse; <0: not an ellipse! (what's that?)

20.2. Rebalanced portfolio#

Let the 1-period return of the assets be normal (todo is this necessary? Can’t one rely on central limit theorem? How long the summation must be for convergence to normal distribution, in presence of heavy-tails distribution? If one can’t rely on central limit theorem, let use numerical methods to investigate the effect of heavy tails distributions),

Compound return of the portfolio has expected value

and variance

20.2.1. Shannon demon#

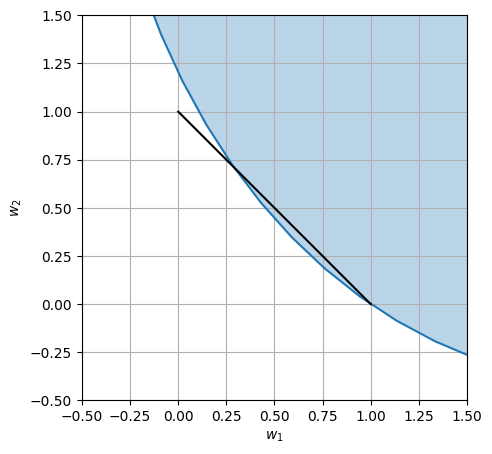

Sometimes the expected value of the compound return of the rebalanced portfolio can be larger than the expected return of each asset class.

Example: 2-asset portfolio. As an example, the expected value of the compund return of a 2-asset rebalanced portfolio,

Using \(w_1\), \(w_2\) as independent variables, for any value of the expected return, the expression of the return itself can be represented as a conic section in the \(w_1,w_2\)-plane. In particular,

for \(\rho \ne 1\), it’s an ellipse (\(\Delta = B^2 - 4 A C < 0\)),

for \(\rho = 1\), it’s a parabola (\(\Delta = 0\))

Portfolio allocation. Some constraints may hold on portfolio allocation:

fully-invested: \(w_1 + w_2 = 1\)

no short-selling: \(w_1,\ w_2 \ge 0\)

no leverage: \(w_1, \ w_2 \le 1\)

Show code cell source

def plot_shannon_demon_set(rho, mu1, sigma1, mu2, sigma2):

#> Plot parameters

xmin, xmax, nx = -10.5, 11.5, 21

ymin, ymax, ny = -10.5, 11.5, 21

#> Expected value of single-asset compound returns

ElnP1 = mu1 - .5 * sigma1**2

ElnP2 = mu2 - .5 * sigma2**2

ElnP = max(ElnP1, ElnP2) # Take max for comparison

#> Define conics coefficients and find points

a, b, c, d, e, f = -.5*sigma1**2, -rho*sigma1*sigma2, -.5*sigma2**2, mu1 ,mu2, -ElnP

ctype, x, y = conics_points(a,b,c,d,e,f, printout=False)

#> Plot

print(f"max(ElnP1, ElnP2): {ElnP}")

fig, ax = plt.subplots(1,1, figsize=(5,5))

ax.plot(x,y)

ax.fill(x,y, alpha=.3)

ax.plot(np.linspace(0,1), np.linspace(1,0), color='black')

ax.grid()

ax.set_aspect('equal') # , 'box')

ax.set_xlim(-.5,1.5)

ax.set_ylim(-.5,1.5)

ax.set_xlabel("$w_1$")

ax.set_ylabel("$w_2$")

#> Initial value of params

mu1 = params['2-asset-portfolio']['mu1']

sigma1 = params['2-asset-portfolio']['sigma1']

mu2 = params['2-asset-portfolio']['mu2']

sigma2 = params['2-asset-portfolio']['sigma2']

rho = params['2-asset-portfolio']['rho']

#> Interactive plot

interact(

plot_shannon_demon_set,

rho=FloatSlider( value=rho , min=-1.0 , max=1.0, step=0.01, description='rho'),

mu1=FloatSlider( value=mu1 , min=-0.30, max=.30, step=0.01, description=f'mu1'),

mu2=FloatSlider( value=mu2 , min=-0.30, max=.30, step=0.01, description=f'mu2'),

sigma1=FloatSlider(value=sigma1, min= .0 , max=.30, step=0.01, description=f'sig1'),

sigma2=FloatSlider(value=sigma2, min= .0 , max=.30, step=0.01, description=f'sig2')

);

This plot represents in blue asset allocations of the balanced 2-asset portfolio with expected value of the compound return larger than the compound return of any individual asset. Black line represents all the possible allocations of a fully invested portfolio, \(w_1+w_2=1\) with no leaverage \(w_k \le 1\) and not short selling \(w_k \ge 0\).

20.3. Comparison of portfolios: realizations of stochastic processes#

In this section, rebalanced portfolio and buy-and-hold portfolio are compared. Different realizations of these two portfolio strategies are built, and used to build statistics, and discuss their properties in terms of compound return, drawdowns,…

Note. Here, 1-period returns are modelled as normal random variable so far. Anyways, it’s possible (and suggested) to implement the most suited random process for modelling the return of the desired assets.

20.3.1. Useful functions#

A useful function is introduced here to build correlated random variables with the desired expected values and covariance.

Main Colab notebook can be found here: https://colab.research.google.com/drive/1n5py0Zf8i3_jrTTk0AR7Noq2kBYwpaqx?authuser=1#scrollTo=gmbjbprjCHto

Show code cell content

def correlated_variable_coeffs(mux, muy, sigmax, sigmay, rhoxy):

if ( np.abs(rhoxy) > 1. ):

raise ValueError('Invalid correlation coefficient, |rhoxy|=|{rhoxy}| > 1.')

elif ( not rhoxy == 1. ):

a = rhoxy * sigmay / sigmax

sigmaz = 1.

b = np.sqrt(sigmay**2 - a**2 * sigmax**2) / sigmaz**2

c = 0.

muz = (muy - c - mux * rhoxy * sigmay / sigmax) / b

else:

a = rhoxy * sigmay / sigmax

muz = 0.

sigmaz = 1.

b = 0.

c = muy - mux * rhoxy * sigmay / sigmax

return muz, sigmaz, a, b, c

20.3.2. Realizations#

Show code cell source

#> Parameters of the 2 assets

mu1 = params['2-asset-portfolio']['mu1'] #

sigma1 = params['2-asset-portfolio']['sigma1'] #

mu2 = params['2-asset-portfolio']['mu2'] #

sigma2 = params['2-asset-portfolio']['sigma2'] #

rho = -.5 # params['2-asset-portfolio']['rho'] #

#> Evaluate the parameters of an independent r.v. Z to build the r.v. of asset 2

# with desired average value, variance and covariance with X

muz, sigmaz, a,b,c = correlated_variable_coeffs(mu1, mu2, sigma1, sigma2, rho)

#> Weights of the 2 assets

# rebalanced ptf : constant weights

# buy-and-hold ptf: initial weights

w1, w2 = 0.5, 0.5

#> Initial conditions

y0 = 1

#> Random number generator, representing 1-period return R_n = Y_{n}/Y_{n-1}

nreal = 1000 # n. of realizations of the random process

nt = 100 # n. of periods (toss) for each realization

tv = np.arange(nt)

#> Random number generators of the 2 assets

rng1 = np.random.default_rng().normal

rng1_params = {'loc': mu1, 'scale': sigma1, 'size': nt}

rngZ = np.random.default_rng().normal

rngZ_params = {'loc': muz, 'scale': sigmaz, 'size': nt}

#> End values, max drawdowns

y_reb_end, y_bah_end = np.zeros(nreal), np.zeros(nreal)

reb_max_drawdown, bah_max_drawdown = np.zeros(nreal), np.zeros(nreal)

fig, ax = plt.subplots(1,2, figsize=(10,5))

for ireal in np.arange(nreal):

#> 1-period returns of the 2 assets

r1 = rng1(**rng1_params)

rZ = rngZ(**rngZ_params)

r2 = a*r1 + b*rZ + c

#> Rebalanced portfolio

y_reb = np.zeros(nt); y_reb[0] = y0

y_reb[1:] = y_reb[0]*np.cumprod(1 + w1*r1[1:] + w2*r2[1:])

#> Buy-and-hold portfolio

y_bah_1 = np.zeros(nt); y_bah_1[0] = y0 * w1

y_bah_2 = np.zeros(nt); y_bah_2[0] = y0 * w2

y_bah_1[1:] = y_bah_1[0]*np.cumprod(1+r1[1:])

y_bah_2[1:] = y_bah_2[0]*np.cumprod(1+r2[1:])

y_bah = y_bah_1 + y_bah_2

#> End values

y_reb_end[ireal] = y_reb[-1]/y0

y_bah_end[ireal] = y_bah[-1]/y0

#> Max drawdowns

y_reb_max = np.maximum.accumulate(y_reb)

y_bah_max = np.maximum.accumulate(y_bah)

reb_drawdowns = 1. - y_reb/y_reb_max

bah_drawdowns = 1. - y_bah/y_bah_max

#> Update stored realization with max drawdown

if np.max(reb_drawdowns) > np.max(reb_max_drawdown):

y_reb_max_drawdown = y_reb.copy()

if np.max(bah_drawdowns) > np.max(bah_max_drawdown):

y_bah_max_drawdown = y_bah.copy()

reb_max_drawdown[ireal] = np.max(reb_drawdowns)

bah_max_drawdown[ireal] = np.max(bah_drawdowns)

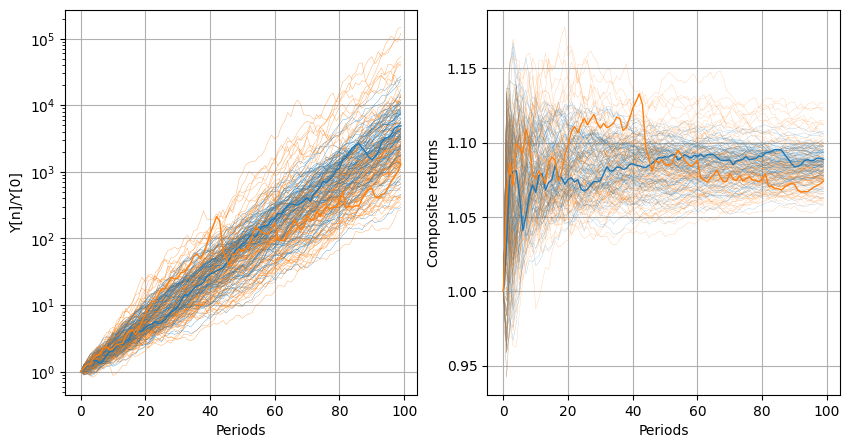

if ( ireal % 10 == 0 ):

ax[0].semilogy(tv, y_reb/y_reb[0], lw=.2, color=plt.cm.tab10.colors[0])

ax[0].semilogy(tv, y_bah/y_bah[0], lw=.2, color=plt.cm.tab10.colors[1])

ax[1].plot(tv, ((y_reb)/y_reb[0])**(1/(tv+1)), lw=.1, color=plt.cm.tab10.colors[0])

ax[1].plot(tv, ((y_bah)/y_bah[0])**(1/(tv+1)), lw=.1, color=plt.cm.tab10.colors[1])

ax[0].set_ylabel("Y[n]/Y[0]")

ax[0].set_xlabel("Periods")

ax[0].grid()

ax[1].set_ylabel("Composite returns")

ax[1].set_xlabel("Periods")

ax[1].grid()

ax[0].semilogy(tv, y_reb_max_drawdown/y_reb[0], lw=1, color=plt.cm.tab10.colors[0], label='Rebalanced')

ax[0].semilogy(tv, y_bah_max_drawdown/y_reb[0], lw=1, color=plt.cm.tab10.colors[1], label='Buy-and-hold')

ax[1].plot(tv, (y_reb_max_drawdown/y_reb[0])**(1/(tv+1)), lw=1, color=plt.cm.tab10.colors[0], label='Rebalanced')

ax[1].plot(tv, (y_bah_max_drawdown/y_reb[0])**(1/(tv+1)), lw=1, color=plt.cm.tab10.colors[1], label='Buy-and-hold')

#> Analytical solution

# logret = expected_logret_fun(b,a,p,f)

# ax.semilogy(tv, y0*np.exp(logret)**tv, lw=1, color=plt.cm.tab10.colors[0])

# ax.set_ylabel("Y[n]/Y[0]")

# ax.set_xlabel("Periods")

# ax.grid()

[<matplotlib.lines.Line2D at 0x7f825f3f6fa0>]

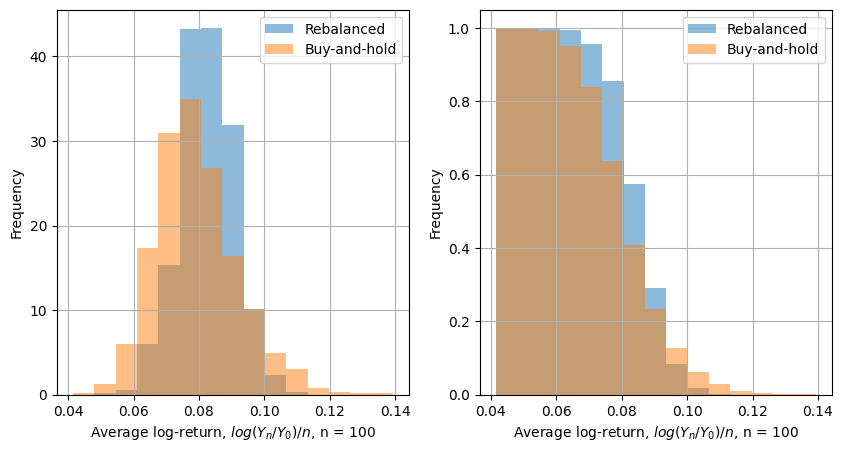

20.3.3. Composite return#

Show code cell source

#> Average and variance of composite return

print("Rebalanced portfolio. Compsite return")

print(f" Exp. value: {np.mean((y_reb_end/y0)**(1/nt)-1):.3f}")

print(f" Std. dev. : {np.std( (y_reb_end/y0)**(1/nt)-1):.3f}")

print("Buy-and-Hold portfolio. Compsite return")

print(f" Exp. value: {np.mean((y_bah_end/y0)**(1/nt)-1):.3f}")

print(f" Std. dev. : {np.std( (y_bah_end/y0)**(1/nt)-1):.3f}")

fig, ax = plt.subplots(1,2, figsize=(10,5))

#> Define hist bins

min_logret = min(np.min(np.log(y_reb_end/y0)/nt), np.min(np.log(y_bah_end/y0)/nt))

max_logret = max(np.max(np.log(y_reb_end/y0)/nt), np.max(np.log(y_bah_end/y0)/nt))

nbins = 15

min_bins = min_logret - (max_logret - min_logret)/nbins

max_bins = max_logret + (max_logret - min_logret)/nbins

bins = np.linspace(min_bins, max_bins, nbins+1)

#> Loop over density and cumulative probability

cum_v = [False, -1]

for i in range(2):

ax[i].hist(np.log(y_reb_end/y0)/nt, bins=bins, density=True, cumulative=cum_v[i], alpha=.5, label="Rebalanced")

ax[i].hist(np.log(y_bah_end/y0)/nt, bins=bins, density=True, cumulative=cum_v[i], alpha=.5, label="Buy-and-hold")

ax[i].set_xlabel(f"Average log-return, $log(Y_n/Y_0)/n$, n = {nt}")

ax[i].set_ylabel("Frequency")

ax[i].legend(); ax[i].grid()

Rebalanced portfolio. Compsite return

Exp. value: 0.086

Std. dev. : 0.009

Buy-and-Hold portfolio. Compsite return

Exp. value: 0.083

Std. dev. : 0.014

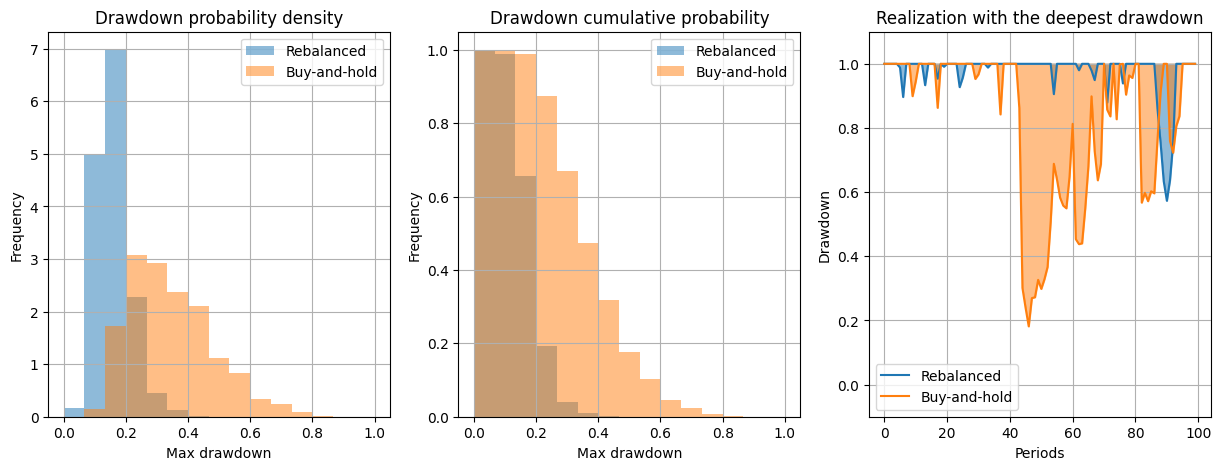

20.3.4. Maximum drawdown#

Show code cell source

fig, ax = plt.subplots(1,3, figsize=(15,5))

#> Define hist bins

# min_drawdown = min(np.min(y_reb_max_drawdown), np.min(y_bah_max_drawdown))

# max_drawdown = min(np.max(y_reb_max_drawdown), np.max(y_bah_max_drawdown))

nbins = 15

min_bins = 0. # min_drawdown - (max_drawdown - min_drawdown)/nbins

max_bins = 1. # max_drawdown + (max_drawdown - min_drawdown)/nbins

bins = np.linspace(min_bins, max_bins, nbins+1)

cum_v = [False, -1]

for i in range(2):

ax[i].hist(reb_max_drawdown, bins=bins, alpha=.5, density=True, cumulative=cum_v[i], label="Rebalanced")

ax[i].hist(bah_max_drawdown, bins=bins, alpha=.5, density=True, cumulative=cum_v[i], label="Buy-and-hold")

ax[i].set_xlabel(f"Max drawdown")

ax[i].set_ylabel("Frequency")

ax[i].legend(); ax[i].grid()

#> Drawdowns as a function of time for the realization with deepest drawdown

reb_running_max = np.maximum.accumulate(y_reb_max_drawdown)

bah_running_max = np.maximum.accumulate(y_bah_max_drawdown)

ddown_reb = 1. - y_reb_max_drawdown/reb_running_max

ddown_bah = 1. - y_bah_max_drawdown/bah_running_max

ax[2].plot(tv, 1.-ddown_reb, color=plt.cm.tab10.colors[0], label='Rebalanced')

ax[2].plot(tv, 1.-ddown_bah, color=plt.cm.tab10.colors[1], label='Buy-and-hold')

ax[2].fill_between(tv, 1.-ddown_reb, np.ones(nt), color=plt.cm.tab10.colors[0], alpha=.5)

ax[2].fill_between(tv, 1.-ddown_bah, np.ones(nt), color=plt.cm.tab10.colors[1], alpha=.5)

ax[2].set_xlabel("Periods")

ax[2].set_ylabel("Drawdown")

ax[2].set_ylim(-.1, 1.1)

ax[2].legend()

ax[2].grid()

ax[0].set_title("Drawdown probability density")

ax[1].set_title("Drawdown cumulative probability")

ax[2].set_title("Realization with the deepest drawdown")

Text(0.5, 1.0, 'Realization with the deepest drawdown')